Content Summary

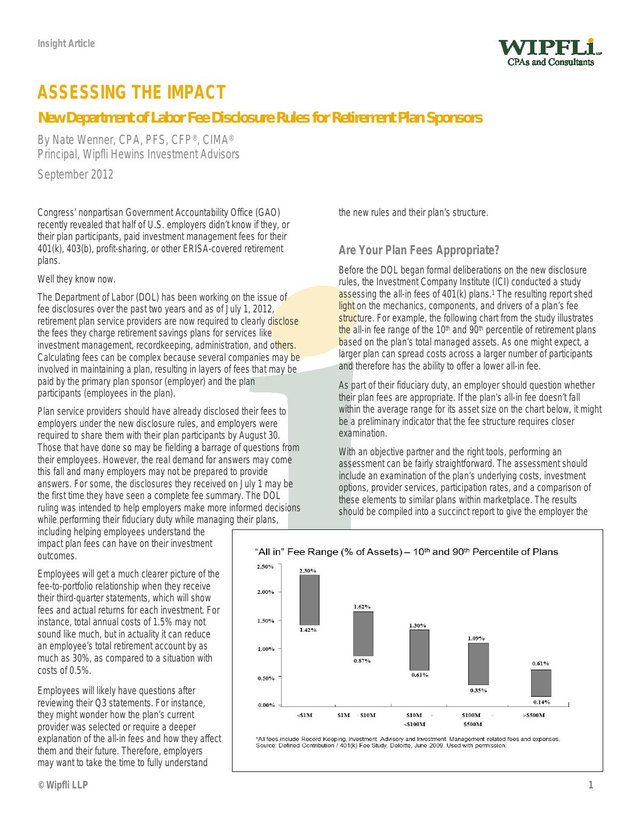

The Department of Labor (DOL) has been working on the issue of fee disclosures over the past two years and as of July 1, 2012, retirement plan service providers are now required to clearly disclose the fees they charge retirement savings plans for services like investment management, recordkeeping, administration, and others. Calculating fees can be complex because several companies may be involved in maintaining a plan, resulting in layers of fees that may be paid by the primary plan sponsor (employer) and the plan participants (employees in the plan).

Access this content

Choose an option below

Your content has been opened.

Register to access this content

Verify your email to access this content

Code sent. Enter it in the modal

Your content has been opened.

Why do I need to verify I’m human?

Please verify you are a human before opening this content.

Your content has been opened.

The content will open in a new window. You may need to allow popups for this site.

Check your inbox

Assessing the Impact: New DOL Fee Disclosure Rules for Retirement Plan Sponsors has been emailed to . Entered the wrong email?

Don't see the content in your inbox?

Make sure to check your spam and other messages folders.

Can't get to your email right now?

By accessing content on the Insurance & Technology Online Buyer's Guide you agree to our Terms of Service and Privacy Policy; and, you acknowledge that your information may be shared with the content publisher.

You might also be interested in

The Rise of AI Review Boards

As Artificial Intelligence moves from experimentation into everyday business operations, organizations in Insurance and Human Resources are facing a new governance challenge: how...

Read More

The Most Efficient and Compliant Temporary Vehicle Registration with Quick Tags by Fairfax Software

We at Fairfax Software are proud to offer innovative solutions like Quick Tags and Quick Snippet that streamline your business operations and improve efficiency. Our Quick Tags...

Read More

Data Migration for Insurance Agencies: Challenges, Strategies and Techniques

Embarking on digital transformation is a challenging yet essential endeavor for insurance agencies aiming to enhance their operational efficiency, customer satisfaction, and...

Read More